Discover Turkey’s tax incentives for foreign investors including investment certificates, technology zones, free trade zones, and R&D benefits.

Introduction to Turkey’s Investment Incentive Framework

Foreign companies considering Turkey as an investment destination often ask about available tax incentives. The answer is encouraging; Turkey offers one of the world’s most comprehensive incentive frameworks, capable of reducing effective tax rates to near zero for qualifying activities.

The Turkish government has designed these incentives to attract foreign direct investment, promote regional development, and support strategic industries. Whether you are establishing a company in Turkey for manufacturing, technology development, or export operations, understanding available incentives can significantly impact your investment decision and bottom line.

Turkey’s incentive system operates through multiple channels. Investment incentive certificates provide tiered benefits based on location and sector. Technology development zones offer complete tax exemption for R&D activities. Free trade zones exempt manufacturers from corporate tax on export revenues. R&D centers deliver substantial deductions outside designated zones. Each program carries specific eligibility requirements and application procedures.

Recent legislative changes have modified some incentive structures. The 2025 domestic minimum tax affects certain incentive calculations, while free zone benefits now apply exclusively to export revenues. These developments make professional legal guidance essential when structuring investments to maximize available benefits.

Investment Incentive Certificate System

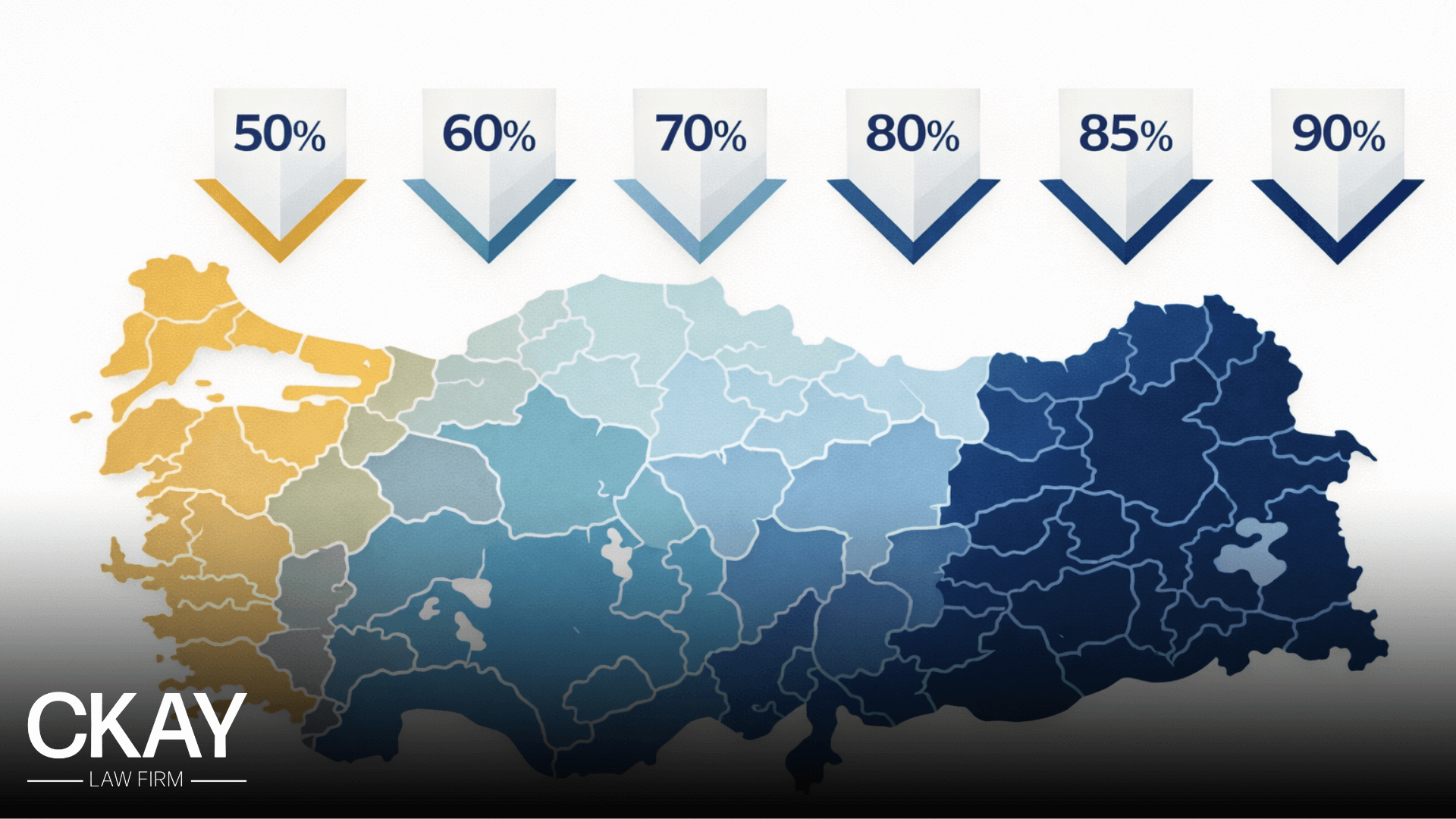

The investment incentive certificate, known as “Yatirim Tesvik Belgesi“, forms the cornerstone of Turkey’s regional development strategy. This system divides the country into six regions, with incentives increasing as development levels decrease.

Foreign investors receive equal treatment with domestic companies under this framework. No restrictions apply based on nationality or foreign ownership percentage. The system rewards investments in less-developed eastern regions while still providing meaningful benefits in developed western areas.

Regional Classification

Turkey’s six-region classification determines available incentive levels. Region 1 encompasses the most developed provinces, while Region 6 covers the least developed areas requiring maximum support.

- Region 1 includes Istanbul, Ankara, Izmir, Bursa, Kocaeli, and other major economic centers. These areas receive baseline incentives reflecting their established infrastructure and workforce availability.

- Regions 2 through 5 offer progressively enhanced benefits. Mid-tier provinces like Adana, Gaziantep, Kayseri, and Konya fall within these categories, balancing development potential with incentive generosity.

- Region 6 covers eastern provinces including Agri, Ardahan, Bingol, Bitlis, Hakkari, Mus, Sirnak, and Van. These areas receive maximum incentives to stimulate economic activity and job creation.

Available Incentives By Region

The incentive package varies significantly across regions. Understanding these differences helps investors optimize location decisions based on operational requirements and tax benefits.

Corporate tax reduction rates by region:

- Region 1: 50% reduction (effective rate 12.5%),

- Region 2: 55% reduction (effective rate 11.25%),

- Region 3: 60% reduction (effective rate 10%),

- Region 4: 70% reduction (effective rate 7.5%),

- Region 5: 80% reduction (effective rate 5%),

- Region 6: 90% reduction (effective rate 2.5%).

Investment contribution rates determine total available tax savings:

- Region 1: 15% of investment amount,

- Region 2: 20% of investment amount,

- Region 3: 25% of investment amount,

- Region 4: 30% of investment amount,

- Region 5: 40% of investment amount,

- Region 6: 50% of investment amount.

All regions receive VAT exemption on domestic machinery and equipment purchases. Customs duty exemption applies to imported machinery and equipment. These exemptions apply regardless of regional classification.

Social security premium support duration varies:

- Region 1: 2 years employer share support,

- Region 2: 3 years employer share support,

- Region 3: 5 years employer share support,

- Region 4: 6 years employer share support,

- Region 5: 7 years employer share support,

- Region 6: 10 years employer share support plus employee share support.

Organized Industrial Zone Bonus

Investments within Organized Industrial Zones (OIZs) qualify for benefits of one region higher than their geographic location. A manufacturing facility in a Region 3 OIZ receives Region 4 incentive rates. This bonus makes OIZ locations particularly attractive for foreign investors seeking enhanced benefits in accessible areas.

OIZs also provide additional advantages beyond tax incentives. Ready infrastructure, streamlined permitting, and concentrated supplier networks reduce operational complexity. Property tax exemptions for 5 years and VAT-free land purchases further improve the investment case.

Minimum Investment Thresholds

Qualifying for investment incentive certificates requires meeting minimum investment amounts. These thresholds vary by region to ensure incentives flow to meaningful investments.

Minimum fixed investment requirements:

- Regions 1-2: TRY 1 million,

- Regions 3-6: TRY 500,000.

Strategic investments and priority sector investments may have different thresholds. Large-scale investments exceeding specific amounts qualify for enhanced “strategic investment” status with additional benefits.

Technology Development Zones

Turkey’s Technology Development Zones, commonly called “Teknoparks”, offer the most generous tax incentives available. Over 92 active zones host more than 11,500 companies engaged in research, development, and software activities.

These zones specifically target technology and innovation. Software development, R&D projects, and design activities conducted within zone boundaries qualify for comprehensive exemptions. The framework supports Turkey’s goal of transitioning toward a knowledge-based economy.

Corporate Tax Exemption

Companies operating within Technology Development Zones enjoy 100% corporate tax exemption on profits from qualifying activities. This exemption remains valid until December 31, 2028, providing long-term planning certainty for investors.

Qualifying activities include:

- Research and development projects,

- Software development and coding,

- Design activities,

- Technology transfer and licensing.

The exemption applies to profits derived from these activities, not to all company income. Companies must maintain separate accounting for zone activities when conducting both qualifying and non-qualifying operations.

Technology sales, transfers, and licensing require intellectual property registration to maintain exemption eligibility. Patents, utility models, design registrations, or copyright protection must be secured for the relevant technology.

Personnel Income Tax Exemption

Zone companies benefit from substantial income tax exemptions on R&D personnel salaries. The exemption rates vary based on employee qualifications, rewarding investment in highly educated talent.

Income tax exemption rates:

- PhD holders or Master’s graduates in supported programs; 95% exemption,

- Master’s or Bachelor’s graduates in supported programs; 90% exemption,

- All other R&D personnel; 80% exemption.

A cap of 40 times the gross minimum wage per period limits the exemption amount. This ceiling prevents unlimited benefits on extremely high salaries while maintaining substantial advantages for most compensation levels.

Social Security Premium Support

The government covers 50% of employer social security contributions for qualifying R&D staff. This support applies for up to five years per employee, reducing ongoing labor costs significantly.

Support personnel cannot exceed 10% of full-time R&D employees under this program. Companies with 15 or fewer R&D employees may include support personnel up to 20% of the R&D headcount.

Additional Zone Benefits

Beyond income tax advantages, Technology Development Zones provide additional benefits that enhance their attractiveness.

Additional incentives include:

- VAT exemption on software deliveries,

- Customs duty exemption on R&D equipment imports,

- Stamp tax exemption on R&D-related documents,

- 100% remote work now permitted for IT personnel.

Major zones include Teknopark Istanbul, ITU Ari Teknokent, METU Technopolis, Bilkent Cyberpark, and ODTU Teknokent. Each zone offers slightly different facilities, support services, and sector focuses. Foreign investors should evaluate zone characteristics against their specific operational requirements.

Free Trade Zones

Turkey operates 19 active Free Trade Zones offering comprehensive exemptions for export-focused operations. These zones function as customs-free territories where manufacturing and trading activities benefit from preferential tax treatment.

The free zone framework particularly suits companies serving international markets from a Turkish base. Geographic positioning between Europe, Middle East, and Asia makes Turkish free zones attractive for regional distribution and manufacturing operations.

Corporate Tax Exemption For Manufacturers

Manufacturers operating in free zones enjoy 100% corporate tax exemption on export revenues. This exemption remains valid until Turkey achieves full European Union membership, providing extended planning horizons for long-term investments.

- Critical 2025 Change: The exemption now applies exclusively to export revenues. Domestic sales profits face the standard 25% corporate tax rate. This modification requires careful revenue planning for companies serving both export and domestic markets.

Non-manufacturing users with operating licenses obtained after February 6, 2004, do not qualify for corporate tax exemption. Trading and service companies should verify their license date and activity classification before assuming exemption eligibility.

Employee Income Tax Exemption

Free zone employees qualify for income tax exemption when their employer exports 85% or more of FOB value of goods produced. Meeting this threshold requires careful monitoring of export ratios throughout the year.

Companies falling below the 85% threshold lose employee income tax exemption for that period. Planning production and sales to maintain the required export percentage helps preserve this valuable benefit.

Operating License Duration

Free zone operating licenses provide long-term operational security. License durations vary based on user type and investment level.

License durations:

- Tenant Users: 15 years,

- Manufacturer-investors: Up to 45 years,

- Land lease on Treasury Property: Up to 49 years.

Major free zones include Mersin FTZ (Turkey’s first zone, focused on maritime trade), Aegean FTZ in Izmir (electronics, automotive, textiles), Istanbul Thrace FTZ (manufacturing, logistics, European access), and Bursa FTZ (automotive, textiles).

R&D and Design Center Incentives

Companies conducting R&D activities outside Technology Development Zones can still access substantial incentives through the R&D Center framework. Law No. 5746 provides tax deductions and social security support for qualifying centers.

This option suits companies unable or unwilling to relocate to designated zones. Existing facilities can qualify by meeting minimum personnel requirements and establishing dedicated R&D operations.

R&D Tax Deduction

Qualifying R&D centers may deduct 100% of eligible R&D expenditures from their corporate tax base. This deduction applies in addition to normal expense deduction, effectively creating a super-deduction for R&D spending.

An additional 50% deduction applies when R&D spending increases by 20% or more from the previous year. Meeting improvement thresholds in patents, international projects, or new product turnover ratio also triggers the enhanced deduction.

Minimum Personnel Requirements

Establishing a qualifying R&D or Design Center requires meeting minimum staffing thresholds. These requirements ensure incentives flow to genuine research operations rather than administrative relabeling.

Minimum full-time equivalent personnel:

- R&D Centers: 15 FTE R&D personnel,

- Design Centers: 10 FTE design personnel,

- Motor Vehicles, Aircraft, and Spacecraft Sectors: 30 FTE personnel.

Personnel must work exclusively on R&D or design activities. Administrative and support staff do not count toward minimum thresholds but may qualify for certain benefits once the center is established.

Personnel Income Tax Exemption

R&D and Design Center personnel qualify for income tax exemptions mirroring Technology Development Zone rates. PhD holders receive 95% exemption, Master’s degree holders receive 90%, and others receive 80%.

Venture Capital Obligation

Taxpayers claiming R&D deductions or corporate tax exemptions exceeding TRY 2 million must invest 3% of the benefit amount in venture capital. This requirement supports Turkey’s startup ecosystem while capping individual obligations at TRY 100 million.

Employment and Social Security Incentives

Beyond investment-specific incentives, Turkey provides general employment incentives that foreign companies can access. These programs reduce ongoing labor costs and reward job creation.

Employer SGK Discount

Companies maintaining timely social security payment compliance qualify for a 5% discount on employer contributions. This automatic benefit rewards administrative compliance without requiring separate applications.

The discount reduces effective employer rates from 20.75% to approximately 15.75% for qualifying companies. Manufacturing sector employers receive an additional 5-point reduction through sector-specific programs.

Regional Employment Support

Employment incentives increase from Region 1 to Region 6, paralleling the investment incentive structure. Region 6 employers may receive up to 10 years of employer share support plus additional employee share support.

Additional employment incentives:

- Youth employment programs for workers under 29,

- SGK contribution waivers for limited periods through ISKUR programs,

- Discounted premiums for hiring registered disabled workers,

- Additional support for female employment in certain sectors.

Double Taxation Agreements

Turkey’s extensive double taxation agreement network provides significant benefits for foreign investors. Treaties with over 80 countries reduce withholding taxes and prevent double taxation of cross-border income.

Withholding Tax Reductions

Standard Turkish withholding rates often decrease substantially under applicable treaties. Dividend withholding of 15% may reduce to 5-10% under many agreements. Interest withholding of 10% frequently drops to 5-7.5%. Royalty withholding of 20% typically decreases to 5-10%.

Key treaty partners include:

- United States, United Kingdom, Germany, France, Netherlands,

- China, Japan, South Korea, India, Singapore,

- UAE, Saudi Arabia, Qatar, Kuwait,

- Russia, Poland, Romania, Hungary, Czech Republic,

- All major OECD economies.

Accessing Treaty Benefits

Treaty benefits require proper documentation and compliance with beneficial ownership requirements. Residence certificates from home country tax authorities establish treaty eligibility. Beneficial ownership declarations confirm the recipient genuinely owns the income rather than acting as a conduit.

Conduit arrangements lacking genuine economic substance face scrutiny. Tax authorities increasingly challenge structures designed solely to access favorable treaty rates without underlying business purpose.

Sector-Specific Incentives

Certain industries receive enhanced incentives reflecting strategic importance to Turkey’s economic development goals. Understanding sector-specific programs helps investors in these areas maximize available benefits.

Technology and Software

Beyond Technology Development Zone benefits, the software sector enjoys reduced withholding on certain payments and preferential treatment under various programs. Istanbul Finans Teknopark specifically targets fintech companies seeking zone benefits.

Renewable Energy

Turkey’s YEKDEM feed-in tariff system provides 10-15 year guaranteed tariffs for renewable energy producers. Priority investment status qualifies renewable projects in developed regions for less-developed region incentive rates.

Equipment localization requirements apply to YEKA tenders, creating opportunities for domestic manufacturing investments. Substantial battery production and EV production incentives support the broader clean energy transition.

Tourism

Accommodation services benefit from reduced 8% VAT rates. A 2% accommodation tax applies with 50% reduction available for promoted tourism categories including winter, thermal, health, rural, and qualified sports tourism.

Manufacturing

Manufacturing investments qualify for the full range of regional incentives plus sector-specific support. OIZ location bonuses, reduced social security rates, and priority sector designations enhance manufacturing investment returns.

How to Access These Incentives

Securing available incentives requires proper application procedures and ongoing compliance. Understanding the process helps foreign investors capture maximum benefits from their Turkish investments.

Investment Incentive Certificate Application

Applications for investment incentive certificates go through the Ministry of Industry and Technology. The process requires detailed investment plans, feasibility studies, and supporting documentation. Processing typically takes 2-4 weeks for straightforward applications.

Required documentation includes:

- Investment project details and timeline,

- Feasibility study demonstrating economic viability,

- Employment projections,

- Environmental impact assessments where applicable,

- Company registration documents.

Technology Zone Application

Establishing operations in a Technology Development Zone requires zone management approval. Each zone maintains its own application process, evaluation criteria, and space availability. Early engagement with target zones helps secure preferred locations.

Professional Guidance

The complexity of Turkey’s incentive framework makes professional guidance valuable. Experienced Turkish Tax Law professionals help investors identify applicable incentives, structure investments optimally, and maintain ongoing compliance with program requirements.

Proper structuring at the investment stage prevents costly restructuring later. Tax advisors familiar with both Turkish requirements and investor home country implications provide comprehensive planning support.

Maximizing Your Investment Returns in Turkey

Turkey’s tax incentives for foreign companies rank among the world’s most generous. The combination of regional investment certificates, technology zone exemptions, free trade zone benefits, and R&D incentives creates legitimate pathways to dramatically reduce effective tax rates.

The 2024-2025 reform cycle introduced important modifications. The domestic minimum tax, revised free zone rules, and global minimum tax compliance affect how sophisticated investors structure their operations. These changes make current professional advice essential rather than optional.

For foreign investors evaluating Turkey, the incentive framework represents a significant competitive advantage. Strategic location between Europe, Asia, and the Middle East combines with meaningful tax benefits to create compelling investment cases across manufacturing, technology, and export-oriented sectors.

Success requires matching business requirements with available programs. Manufacturing operations may benefit most from regional incentives and OIZ locations. Technology companies should evaluate Technology Development Zone options. Export-focused businesses might find free trade zones optimal. Often, combinations of programs deliver maximum benefit.

The key lies in understanding options before committing to specific structures. Early planning captures opportunities that become difficult or impossible to access after investment decisions are finalized.

Frequently Asked Questions (FAQs)

Foreign investors commonly ask these questions about tax incentives in Turkey. Here are concise answers to help guide your investment planning.

What is the corporate tax exemption in Turkish Technology Zones?

Companies in Technology Development Zones receive 100% corporate tax exemption on R&D, software, and design activities until December 31, 2028.

How much can regional investment incentives reduce corporate tax?

Regional incentives reduce corporate tax by 50-90% depending on location. Region 6 investments pay as low as 2.5% effective corporate tax rate.

Do free trade zones still offer tax exemption in 2025?

Yes, but only on export revenues. The 2025 changes limit corporate tax exemption to export sales, with domestic sales taxed at the standard 25% rate.

What is the minimum investment for incentive certificates?

Minimum fixed investment is TRY 1 million for Regions 1-2 and TRY 500,000 for Regions 3-6.

How many R&D personnel are required for an R&D Center?

R&D Centers require minimum 15 full-time equivalent R&D personnel. Design Centers require 10 FTE personnel.

Does Turkey have double taxation agreements?

Yes, Turkey has treaties with over 80 countries that reduce withholding taxes on dividends, interest, and royalties.

Can foreign companies access the same incentives as Turkish companies?

Yes, foreign investors receive equal treatment with no restrictions based on nationality or foreign ownership percentage.

How long do Technology Zone tax exemptions last?

The current exemption period extends until December 31, 2028. Legislative extensions may occur as the deadline approaches.